Friday, May 30, 2008

Tuesday, May 27, 2008

Monday, May 26, 2008

Periodic Functions

In the first part of class this morning we went over what we learned last class (Friday). After that we finished up about the role of Parameter B & the role of Parameter C. The pictures below are pretty straight forward on how it works & how to get it.

Okay, the picture above...I bet your wondering what does the 2 (or any #) in front of the X does!? It helps you find the period....Remember it's not the period it just helps you find it!

After that we went over are homework. Now, I give honors to the next scribe....and they are........ICKIE!!!!!

Friday, May 23, 2008

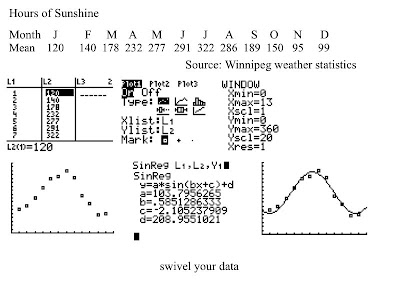

Using sine for patterns

Using SinReg for to figure out patterns is a useful feature. First of all, you need to enter the data into a statplot. Let us say for instance we are calculating the time we have of sunshine each month.

The order of the data that we will get starting after the data given of sunshine is, step 1. the list, step 2.the graph settings, step 3. the V-Win option, step 4. the graph with no line, step 5. the the SinReg list, step 6. the graph with the line.

Step 1.In order to make the list with the sunshine data, you enter the months of the year in list number 1 (ex. January = 1, Febuary = 2, March = 3, etc.). Next, you enter the data for each month into the second list (ex. January = 120, Febuary = 140, March = 178, etc). Once you are finished putting in the list data for each month, you will adjust your graph settings in step 2.

Step 2. you want to set up the data to display a scatter plot. The x and y would be list one and list two (in that order). Any data point can be used for your preferences (Mr.K likes to use the squares).

Step 3. in order to get a good view of the data, you want to set up your V-Win so it goes beyond the data point of of the highest and lowest x and y values. Do not set it up too far or else the data will be squashed.

Step 4. Press the graph button to acheive this data ( must do step 1 though 3 first).

Step 5. go to the calc menu, press reg, and scale down until you reach SinReg. you press it and you should get this formula (refer to the picture).

Step 6. You copy Sinreg to the graph menu. After you get to the graph screen, you must put in beside SinReg L1, L2, Y1. Press graph to get this step. The pattern is likely to continue the next year so now you have a approx. pattern (will never get line exactly with dot). SinReg is useful when getting patterns in a series of data within a certain time period.

The order of the data that we will get starting after the data given of sunshine is, step 1. the list, step 2.the graph settings, step 3. the V-Win option, step 4. the graph with no line, step 5. the the SinReg list, step 6. the graph with the line.

Step 1.In order to make the list with the sunshine data, you enter the months of the year in list number 1 (ex. January = 1, Febuary = 2, March = 3, etc.). Next, you enter the data for each month into the second list (ex. January = 120, Febuary = 140, March = 178, etc). Once you are finished putting in the list data for each month, you will adjust your graph settings in step 2.

Step 2. you want to set up the data to display a scatter plot. The x and y would be list one and list two (in that order). Any data point can be used for your preferences (Mr.K likes to use the squares).

Step 3. in order to get a good view of the data, you want to set up your V-Win so it goes beyond the data point of of the highest and lowest x and y values. Do not set it up too far or else the data will be squashed.

Step 4. Press the graph button to acheive this data ( must do step 1 though 3 first).

Step 5. go to the calc menu, press reg, and scale down until you reach SinReg. you press it and you should get this formula (refer to the picture).

Step 6. You copy Sinreg to the graph menu. After you get to the graph screen, you must put in beside SinReg L1, L2, Y1. Press graph to get this step. The pattern is likely to continue the next year so now you have a approx. pattern (will never get line exactly with dot). SinReg is useful when getting patterns in a series of data within a certain time period.

Thursday, May 22, 2008

BOB

Okay, so for this unit, I think I did pretty well once I got the hang of using the right operations at the right time. The only problem I was having before was that I would subtract or add something at the wrong time, such as when buying a car (when you need to add values before and after you add the taxes). I think I strong point for me was that for the options questions I had a fairly easy time with it because by the time we got to it the only new thing was the common sense added to the answers. Good luck on the test everybody!

BOB - Personal Finance

ok so i think i'm going to do good on this test, i've gone over the notes quite a few times and i feel like i just get scared of the longer questions =\ so hopefully i do ok =)

BOB

This unit was okay for me, it's pretty easy to understand....it's just that there are lots of formulas that you have to remember that I can have trouble with. With the formulas I remember them right now(well, i think so)...but when I get the test I sometimes just blank so then I forget the stuff that I have learn &/or studied. So, I'm hoping that I won't blank out on the test tomorrow!!! That's all that I can think about to write....GOOD LUCK EVERYONE!

BOB

I think i'll do good on the test tomorrow (or in a few hours, depending on what time it is right now). I understood this unit alot more than the past units. Sometimes the answers came to me easily, probably because i remember working on personal finance from grade 11 Applied Math. Like for example, when we first used TVM Solver at the beginning of this unit, it was pretty straightforward to me.

Some things I might have trouble on is questions on mortgage. Theres a lot of information to take in and it gets confusing at times. But then once everything is organized, then the answer is easy to find. For example, the question that involved Lucy Brown who wanted to buy a condo. That was very confusing, mostly because the way the word problems or worded, and i guess i just didnt really read it carefully or understand it well. But seeing the way it was done, it seemed so easy.

Also leasing is a bit of a pain in the butt. There's alot to do, like finding the depreciation, taxing it, down payments, monthly payments, blah blah blah.

Hopefully i do good on this test, right now i feel confident about it, but tests are always surprising.

Wish me luck! :)

(Sorry for the horrible grammar. Hehe. :))

Some things I might have trouble on is questions on mortgage. Theres a lot of information to take in and it gets confusing at times. But then once everything is organized, then the answer is easy to find. For example, the question that involved Lucy Brown who wanted to buy a condo. That was very confusing, mostly because the way the word problems or worded, and i guess i just didnt really read it carefully or understand it well. But seeing the way it was done, it seemed so easy.

Also leasing is a bit of a pain in the butt. There's alot to do, like finding the depreciation, taxing it, down payments, monthly payments, blah blah blah.

Hopefully i do good on this test, right now i feel confident about it, but tests are always surprising.

Wish me luck! :)

(Sorry for the horrible grammar. Hehe. :))

Wednesday, May 21, 2008

BOB

Hey guys, i just finished my scribe post and now im BOB-ing. Well, for this unit, i didn't really have much trouble with it, but i guess, my muddiest point would be the words used in personal finance. I understand taxes and all, but sometimes, some names of deductions are unfamiliar to me and I end up using it differently. My strongest point is that after i break it down, i know where all the numbers go on the calculator! I hope that everyone does well on this test! Goodluck!

BOB - Personal Finance

I'd say this unit was a bit okay for me since I sort of remember a bit of it from applied grade 11.

For me, I feel that I do understand what's happening for the most part, but what has troubled me the most in the unit I think would be the whole process in leasing something. Because you have to find extra things like the residual value, depreciating value, etc.. and I find it a bit hard for myself to just remember how to get those values in order to continue on with the problem. I think I'm good to go with organizing the information on long looking questions though.. so I don't need to worry much about that. But, I tend to second guess myself of whether some certain value goes in which variable spot on the TVM Solver app. Looks like I need to study more.

Good luck everyone.

a[x_x]bc - macs

Periodic Functions

Hey guys this is alvin again with another scribe post!

So what is "Periodic" (Period) really??

--Anything that repeats after a certain/fixed length of time.

Examples

-High tide vs. Low tide

-High tide vs. Low tide

-Heart beat

-Clocks

-Rotation of earth on sun or the Moon on earth

-Rotation of earth on sun or the Moon on earth

...etc.

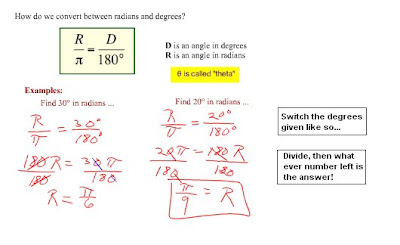

The inner layer are in degreese while the outer fractions with the Pi are radians.

These sets are the most basic angles.

The ratio!

Dealing with negative numbers are a bit different, but not at all difficult. The negative numbers move clockwise while the positive numbers go counter-clockwise (Degrees). But as show on the diagram below, there are 2 ways of getting into the end point. Be careful on what the question is asking or you might end up using a wrong positive/negative number.

Over all, the class today was pretty blunt and covered alot of the stuff. So far its piece-easy, all you really need is to know the ratio, after that, you have a number of options on how to get your answer.

[For any questions, concerns, additions and corrections please leave a comment]

The next scribe is Rennie...?

BOB

Dear Bob,

Tomorrow is the test and I hope I will be doing a good job with it because I have been actually studying harder and harder each day because I want to pass applied math very much and I want to increase my mark. These past 2 weeks we studied about financing a car, computers, mortgages, and making a net worth statement which I really didn't get to learn much about the things I have missed because of the Music trip and my Folk Dance Camp so I'm a bit scared for the test. In the future we're going to have to do all of this to survive and to calculate everything to be able to not be overcharged with things so we save up money and have it a teensy bit easier in life which is why we learnt in math about if we should Lease or buy a Car or Computer or to Rent or Buy a house. One thing I really disliked in this unit is calculating Mortgages I still don't quite understand how to do it properly such as your property after 1, 2, 5, or 10 years. Which is why I shall study and give it my all tonight and tommorow morning to understand how to do the questions that were given to us since day 1 of the Personal Finance Unit. Remember the formulas given to us such as the GDSR, PV of Loan, Equity of House, and Debt/Equity ratio. I hope that's all the formulas given =s maybe something about Net Worth = Assets - Liabilities. Well back to the studying and good luck to all my fellow classmates or to anyone out there who have a quiz, test, or exam to do tommorow^^. David-san signing out(:

Dear Bob,

Tomorrow is the test and I hope I will be doing a good job with it because I have been actually studying harder and harder each day because I want to pass applied math very much and I want to increase my mark. These past 2 weeks we studied about financing a car, computers, mortgages, and making a net worth statement which I really didn't get to learn much about the things I have missed because of the Music trip and my Folk Dance Camp so I'm a bit scared for the test. In the future we're going to have to do all of this to survive and to calculate everything to be able to not be overcharged with things so we save up money and have it a teensy bit easier in life which is why we learnt in math about if we should Lease or buy a Car or Computer or to Rent or Buy a house. One thing I really disliked in this unit is calculating Mortgages I still don't quite understand how to do it properly such as your property after 1, 2, 5, or 10 years. Which is why I shall study and give it my all tonight and tommorow morning to understand how to do the questions that were given to us since day 1 of the Personal Finance Unit. Remember the formulas given to us such as the GDSR, PV of Loan, Equity of House, and Debt/Equity ratio. I hope that's all the formulas given =s maybe something about Net Worth = Assets - Liabilities. Well back to the studying and good luck to all my fellow classmates or to anyone out there who have a quiz, test, or exam to do tommorow^^. David-san signing out(:

BOB

Uhm... today we started the new section, Periodic functions and also finished the Personal Finance. That is not the hard unit but we must be careful when read the question, and remember some formulae :

+GDSR

+PV of Loan ( when we lease a car)

+Equity of house

+Debt/Equity ratio

...I think that's it, ^^ Good luck to u guys and also good luck to me :P

+GDSR

+PV of Loan ( when we lease a car)

+Equity of house

+Debt/Equity ratio

...I think that's it, ^^ Good luck to u guys and also good luck to me :P

BOB FM(Financing w/Math)

Dear Bob FM,

Tomorrow is the test and I hope and getting a higher mark than my last tests so I can bump up my mark a bit.This past 2 weeks we studied about financing a CAR, COMPUTERS, MORTGAGES, and making a NET WORTH STATEMENT. Will we all face all those things in the future for our needs that's why we need to do the math and be smart about whether we should LEASE or BUY a car or computer; or; RENT or BUY a house. The one thing I love about this unit is, we actually apply this to our daily lives and it happens most of the time when we need to purchase something. Budgeting is one thing we need to consider when it comes to financing something we need in order to save alot of money. Also, one thing I unLOVED about this unit was calculating things about MORTGAGES such as your property after 1,2 or 5 years and all that. But, as I study I will most likely learn how to tackle those problems with no sweat. I guess that's all for my BOB FM. Hope we all get high marks in the test and have a nice day. This is BOB FM ,Ace Burpee saying GOOD LUCK with BOB FM.

Tomorrow is the test and I hope and getting a higher mark than my last tests so I can bump up my mark a bit.This past 2 weeks we studied about financing a CAR, COMPUTERS, MORTGAGES, and making a NET WORTH STATEMENT. Will we all face all those things in the future for our needs that's why we need to do the math and be smart about whether we should LEASE or BUY a car or computer; or; RENT or BUY a house. The one thing I love about this unit is, we actually apply this to our daily lives and it happens most of the time when we need to purchase something. Budgeting is one thing we need to consider when it comes to financing something we need in order to save alot of money. Also, one thing I unLOVED about this unit was calculating things about MORTGAGES such as your property after 1,2 or 5 years and all that. But, as I study I will most likely learn how to tackle those problems with no sweat. I guess that's all for my BOB FM. Hope we all get high marks in the test and have a nice day. This is BOB FM ,Ace Burpee saying GOOD LUCK with BOB FM.

Tuesday, May 20, 2008

So today We did practice exercises, which is the reason i volunteered to scribe.

First exercise is calculating the debt/equity ratio. What we do is add all the assets and liabilities.

question 1:

dave's assets:

$100,000 house

$20,000 car

$3,000 in bank

$4,000 near cash

$10,000 mutual funds

$3,000 in Canadian savings bond

$15,000 rrsp

Total=$155,000

Daves Liabilities:

$60,000 mortgage

$15,000 car loan

$4,000 credit card balance

$2,000 loan

total= $81,000

assets-liabilities= net worth

155,000-81,000= 74,000

Now to get the ratio we take liabilities subtract mortgage cause mortgage is one debt we would like to have.

81,000 - 60,000 = 21,000

now we take our liabilities subtract mortgage and divide it by our net worth

81,000-60,000/74,000 = 0.283

so daves liabilities are about 28% of his total net worth

So that was the first question, and the next question already has the answers on the next slide page so i don't think i need to go through it. Oh and our test is on Thursday so get your bob done.

the next scribe will be H20

First exercise is calculating the debt/equity ratio. What we do is add all the assets and liabilities.

question 1:

dave's assets:

$100,000 house

$20,000 car

$3,000 in bank

$4,000 near cash

$10,000 mutual funds

$3,000 in Canadian savings bond

$15,000 rrsp

Total=$155,000

Daves Liabilities:

$60,000 mortgage

$15,000 car loan

$4,000 credit card balance

$2,000 loan

total= $81,000

assets-liabilities= net worth

155,000-81,000= 74,000

Now to get the ratio we take liabilities subtract mortgage cause mortgage is one debt we would like to have.

81,000 - 60,000 = 21,000

now we take our liabilities subtract mortgage and divide it by our net worth

81,000-60,000/74,000 = 0.283

so daves liabilities are about 28% of his total net worth

So that was the first question, and the next question already has the answers on the next slide page so i don't think i need to go through it. Oh and our test is on Thursday so get your bob done.

the next scribe will be H20

BOB

BOB post.... I found this unit pretty easy since it's just like a review from Accounting class; debit and credit, owner's equity etc. The only thing i found abit confusing was when to use the TVMSolver (when to change it from END to BEGIN) I still don't quite understand it, and i hope we can go through it in class. Other than that, all i need to do is look back at my notes.

Net Worth = Assets - Liabilities

Debt/Equity Ratio = (Total Liabilities - Mortgage) / Net Worth

Good luck

Net Worth = Assets - Liabilities

Debt/Equity Ratio = (Total Liabilities - Mortgage) / Net Worth

Good luck

Friday May 16 Scribe Post

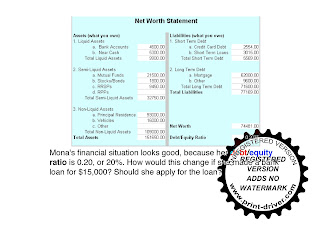

Friday in class we kept looking at Net Worth since we ran out of time last class. Mr. K again explained the different catagories of assests and liabilities there are. We continued on from there by looking at how to calculate your debt/equity ratio which shows how your debts compare to your net worth.

The Total Liabilities for the formula includes all short and long-term debts except for your mortgage as shown in the formula you must subtract from the total liabilities before you divide.

Mr. K also showed us a Net Worth spreadsheet to calculate you debt/equity ratio and Net Worth at the same time where you just type in all the types of assests and liabilities you have in there catagory.

Link: http://tinyurl.com/4x8exe

So after that we did a question on mona wanting to do some extensive house renovations. We used this spredsheet to calculate her debt/equity ratio and net worth in order to see if she was able to get the loan.

.jpg)

We find her debt/equity ratio to come up to 20% but if mona was to get a $15000 loan it would rise up to 51% which means the bank will probably not give her the loan since it is over 50%.

These are 3 tips to raise one's net worth:

1. Get higher rates of return on your investments.

2. Reduce your debts. Remember the more extra money you put on your payments you make on your debts the faster they will reduce.

3. Save more on a regular basis. Save at least 10% of your income. Save before you spend.

Next Scribe: David-san

The Total Liabilities for the formula includes all short and long-term debts except for your mortgage as shown in the formula you must subtract from the total liabilities before you divide.

Mr. K also showed us a Net Worth spreadsheet to calculate you debt/equity ratio and Net Worth at the same time where you just type in all the types of assests and liabilities you have in there catagory.

Link: http://tinyurl.com/4x8exe

So after that we did a question on mona wanting to do some extensive house renovations. We used this spredsheet to calculate her debt/equity ratio and net worth in order to see if she was able to get the loan.

.jpg)

We find her debt/equity ratio to come up to 20% but if mona was to get a $15000 loan it would rise up to 51% which means the bank will probably not give her the loan since it is over 50%.

These are 3 tips to raise one's net worth:

1. Get higher rates of return on your investments.

2. Reduce your debts. Remember the more extra money you put on your payments you make on your debts the faster they will reduce.

3. Save more on a regular basis. Save at least 10% of your income. Save before you spend.

Next Scribe: David-san

Monday, May 19, 2008

Thursday May 15 Scribe Post

So Thursday in class we had a short 3 question quiz that we later went over and corrected:

Question 1 was on emily wishing to obtain a new car. There were 2 options in this question for emily to buy her car, and you have to calculate witch option will cost emily the least.

In question 2 we had to calculate how much a farmers $60000 tractor would be worth after 6 years, at a 8% depreciation rate

per year.

The 3rd question was on a investment of $500 at the beginning of every month, since the payment is at the beginning of each month you have to change PMT from END to BEGIN ( shown in the picture on the left) .

We also went over the homework from the day before with two questions on Mr. T's family moving into another house where we had to find the total additional costs of moving. And Ms. Jonhston buying a home where we had to find if a 20 or 15-year mortgage would be better for her.

We also started learning about net worth(equity) which is the difference between assests and liabilities.

Net Worth = Assests - Liabilities

Assests are everythin of value that you own, and liabilities being any debt you owe.

We learned about the 3 catagories of assests there are: Liquid Assests, Semi-Liquid Assests, and Non-Liquid Assests

And 2 types of Liabilities: Short Term Debts, and Long-Term Debts.

Friday, May 16, 2008

Thursday, May 15, 2008

today May 14

we keep doing some problem :

The Petri Family: A Buy vrs. Rent Case Study The Petri family needs to move, and so they are looking for another home. They are considering buying or renting a home. The price of a suitable home is $125 000. The cost of renting a similar home is $875 per month. They have $21 000 invested in an account that is growing by 7% per year, and they will use this for the down payment and to cover the 'Additional Costs when Purchasing a Home' if they buy. They have also checked with their bank about a mortgage, and they can get a 25-year mortgage at 7.25% to pay for the balance of the home. Other things to consider are:

• the 'Additional Costs when Purchasing a Home' are $6000.00, and so they will have $15 000 for the down payment

• annual property taxes are about 1.5% of the value of the home

• the home is expected to appreciate at 4% per year

• rental payments are also expected to increase 4% per year

• they expect to receive 7% per year growth in their investment if they do not use the $21 000 as a down payment for the home.

1. What is the amount of the monthly mortgage payment?

2. If the property taxes are 1.5% of the market value, how much are property taxes the year they buy the home?After they own the home for 10 years?

***use the home price times 0.015 to find how much taxes for 1 year

***use the home price times 1.04 and power of 10 for 10 years = home with a appreciate for 10 years

***then times 0.015 to find the taxes after 10 years

3. What percent of the first mortgage payment is used to pay interest?

***we'll find the interest of the first payment.

***then / the monthly payment to get the percentage.

4.

5. If the market value of the home increases 4% per year, what is the value of the home after 10 years?

***home price times 1.04 power of 10 cause it's for 10 years

6. If they rented the home for one year at $875 per month, how much would they pay for the year?How much would the annual rental charge be for the 10th year they rent if rental rates increase 4% per year.

***monthly rental charge times 12(12 months in a year)

*** rental charge times 1.04 (the rental rate for a year) power of 10 (10 years)

7. If they rent the house and invest the $21 000 at 7% per year, how large would the investment be after 10 years?

*** TVM solver is good for this.

8. What equity does the Petri family have in the home immediately after buying it? After 2 years? After 3 years?

***∑Prn(1,12); ∑Prn(1,24); ∑Prn(1,36)

9. How do the mortgage payments and rental payments compare during the first year? After 5 years? After 10 years?

*** rental charge times 1.04 power of number of years.

***then - monthly payment of buying.

10. i don't understand question 10........... :( need help

homeworks to do.........

Next scribe is David-san

scribe for May 13

We did some problem in class this morning...

here is one :

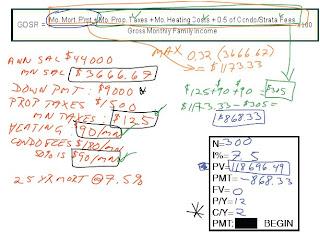

A group of rural students is planning to go to university. One of the members of the group suggests that they purchase an older home rather than rent an apartment. After a careful analysis of their finances, the group decides that their gross monthly income would be around $3000.00. Monthly property taxes are estimated to be $125.00. Heating bills are estimated to be $150.00. The group can arrange a mortgage at a rate of 9%. The three members of the group are able to come up with a down payment of $8000.00. Determine the maximum affordable purchase price that can be considered if they take out a 25-year mortgage.

just have to remember that the mortgage in Canada is compounded twice a year....

the others are mostly the same......

there's some homework too....

i didn't scribe last night so............sorry

i'll scribe for today too!!! :(

here is one :

A group of rural students is planning to go to university. One of the members of the group suggests that they purchase an older home rather than rent an apartment. After a careful analysis of their finances, the group decides that their gross monthly income would be around $3000.00. Monthly property taxes are estimated to be $125.00. Heating bills are estimated to be $150.00. The group can arrange a mortgage at a rate of 9%. The three members of the group are able to come up with a down payment of $8000.00. Determine the maximum affordable purchase price that can be considered if they take out a 25-year mortgage.

just have to remember that the mortgage in Canada is compounded twice a year....

the others are mostly the same......

there's some homework too....

i didn't scribe last night so............sorry

i'll scribe for today too!!! :(

Wednesday, May 14, 2008

Tuesday, May 13, 2008

Monday, May 12, 2008

Student Voices Episode 3: Chris, Craig, and Graeme

In this episode of Student Voices three Advanced Placement Calculus students, Chris, Craig, and Graeme, talk about a wiki assignment they did to prepare for the exam. Then the conversation transitions to a discussion of the many things they learned while doing their Developing Expert Voices project. It ends with a challenge, the result of which will be featured in a future podcast.

Let Chris, Craig, and Graeme know what you thought about the podcast by leaving a comment here on this post or on the mirror of this post on their class blog.

(Download File 31.8Mb, 26 min. 30 sec.)

The video mentioned near the end of the podcast is called Daft Hands. Here it is:

Photo Credit: Shadow singer by flickr user EugeniusD80

Mortgages

Hey everyone! Today we started to learn about mortgages. In the morning class we just mainly talked about the pros & cons about buying or renting homes. The number one pro for buying or renting a home is the LOCATION!! In the afternoon we just talked about costs when purchasing a home.

If you’re renting these are some things that you should keep in mind:

1. You need to pay the monthly rental payments in advance plus probably one month’s rent in advance as damage deposit.

2. It is cheaper to rent a home in the short run than buying, but it doesn’t create any assets.

3. You need to know what is included in the rental payments. Example: are the utilities (especially water, hydro, heating) included? Is the home furnished…etc.

4. When renting a house, the rental payments will increase over time and you don’t create any assets. If you buy a house then the value of the house normally increases with time.

Non-financial factors to consider when renting:

1. When renting you might be restricted to your lifestyle. Example, you maybe not be able to have pets, or modify the home to suit your personal needs.

2. Repairs, maintenance, or property taxes you are not responsible for. Example, if the hot water tank needs replacing, the owner is responsible.

3. It is better to rent then buy a home if you only need the home for a short time. So then you can avoid the inconvenience and expense of reselling the home.

Now, we will look at the costs associated with buying and renting a home.

"How Much Can I Afford to Pay for a Home?"

Banks and other lending institutions have developed a formula that

allows you to calculate the maximum price of a home you can afford.

This formula is known as the Gross Debt Service Ratio, or GDSR.

According to this formula, anyone buying a home should spend no

more than 32% of gross income on household or accommodation

expenses, including mortgage payments, property taxes, heating

and condo/strata fees. The formula may be written as: Question #1

Question #1

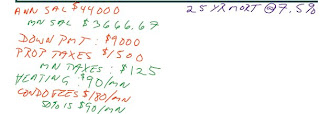

Lucy Brown wants to buy a condo, but does not know how much money she

should spend based on her income. She earns $44 000 per year, and has saved

$9000 for a down payment. The property taxes for the condo she likes are

$1500 per year, and the heating costs average $90 per month. The condo/strata

fees are $180 per month. The bank will give her a 25-year mortgage at an

interest rate of 7.5%. What is the maximum price she can afford for a condo,

based on spending no more than 32% of her gross income on household and

accommodation expenses?

Now since there is so much stuff in the question just break it down into small parts like it is done below.

I know that you are probably wondering why C/Y is 2. Well it is 2 because by law in Canada the bank can ONLY compound you twice a year!

After you calculated everything your Present Value will be $118,696.49 after 25 years. Plus you have to include the $9000 down payment that Lucy has saved up. (Showed below)

I know that you might be wondering what do some of these mean...right down below are some of the definitions.

1. Appraisal fees- The process through which conclusions of property value are obtained; also refers to the report that sets forth the process of estimation and conclusion of value.

2. Property survey- The process by which boundaries are measured and land areas are determined; usually performed by a land surveyor.

3. Insurance costs for high ratio mortgages- This is only for first time house buyers, you only pay 5% of it & the bank pays the rest.

4. Land transfer tax- A tax payable to the Provincial Government by the purchaser upon the transfer of title from a seller.

5. Interest adjustments- Extra proceeds going to an investor who submits a convertible bond for conversion to account for interest accrued since the last date of record for an interest payment.

6. Legal fees- A fee paid for legal service.

I hope you guys like my scribe post & I'm sorry if the pictures arent that good….but now I’m off on my choir & vocal jazz trip to moose jaw! I am honored to announce that our next scribe post will be by the one the only H20!!!!! YEAH.

If you’re renting these are some things that you should keep in mind:

1. You need to pay the monthly rental payments in advance plus probably one month’s rent in advance as damage deposit.

2. It is cheaper to rent a home in the short run than buying, but it doesn’t create any assets.

3. You need to know what is included in the rental payments. Example: are the utilities (especially water, hydro, heating) included? Is the home furnished…etc.

4. When renting a house, the rental payments will increase over time and you don’t create any assets. If you buy a house then the value of the house normally increases with time.

Non-financial factors to consider when renting:

1. When renting you might be restricted to your lifestyle. Example, you maybe not be able to have pets, or modify the home to suit your personal needs.

2. Repairs, maintenance, or property taxes you are not responsible for. Example, if the hot water tank needs replacing, the owner is responsible.

3. It is better to rent then buy a home if you only need the home for a short time. So then you can avoid the inconvenience and expense of reselling the home.

Now, we will look at the costs associated with buying and renting a home.

"How Much Can I Afford to Pay for a Home?"

Banks and other lending institutions have developed a formula that

allows you to calculate the maximum price of a home you can afford.

This formula is known as the Gross Debt Service Ratio, or GDSR.

According to this formula, anyone buying a home should spend no

more than 32% of gross income on household or accommodation

expenses, including mortgage payments, property taxes, heating

and condo/strata fees. The formula may be written as:

Question #1Lucy Brown wants to buy a condo, but does not know how much money she

should spend based on her income. She earns $44 000 per year, and has saved

$9000 for a down payment. The property taxes for the condo she likes are

$1500 per year, and the heating costs average $90 per month. The condo/strata

fees are $180 per month. The bank will give her a 25-year mortgage at an

interest rate of 7.5%. What is the maximum price she can afford for a condo,

based on spending no more than 32% of her gross income on household and

accommodation expenses?

Now since there is so much stuff in the question just break it down into small parts like it is done below.

Once you have done that you can finish answering the question…..like done below.

I know that you are probably wondering why C/Y is 2. Well it is 2 because by law in Canada the bank can ONLY compound you twice a year!

After you calculated everything your Present Value will be $118,696.49 after 25 years. Plus you have to include the $9000 down payment that Lucy has saved up. (Showed below)

I know that you might be wondering what do some of these mean...right down below are some of the definitions.

1. Appraisal fees- The process through which conclusions of property value are obtained; also refers to the report that sets forth the process of estimation and conclusion of value.

2. Property survey- The process by which boundaries are measured and land areas are determined; usually performed by a land surveyor.

3. Insurance costs for high ratio mortgages- This is only for first time house buyers, you only pay 5% of it & the bank pays the rest.

4. Land transfer tax- A tax payable to the Provincial Government by the purchaser upon the transfer of title from a seller.

5. Interest adjustments- Extra proceeds going to an investor who submits a convertible bond for conversion to account for interest accrued since the last date of record for an interest payment.

6. Legal fees- A fee paid for legal service.

I hope you guys like my scribe post & I'm sorry if the pictures arent that good….but now I’m off on my choir & vocal jazz trip to moose jaw! I am honored to announce that our next scribe post will be by the one the only H20!!!!! YEAH.

Sunday, May 11, 2008

Hello, im VERY SORRY about the late post..hope your not mad =)

aaanyways, here's the scribe from FRIDAY MAY 9, 2008.

The answers for D&E are basically your personal opinion.

We worked on a group problem similar to the problem on thursday. Which can be found on slide 9. =D

The lucky winner of the next scribe post will be ........................................

VANESSA!! *the crowd roars* WOO HOO!

aaanyways, here's the scribe from FRIDAY MAY 9, 2008.

We went over the homework from THURSDAY MAY 8, 2008

The answers for D&E are basically your personal opinion.

We worked on a group problem similar to the problem on thursday. Which can be found on slide 9. =D

The lucky winner of the next scribe post will be ........................................

VANESSA!! *the crowd roars* WOO HOO!

Friday, May 9, 2008

Thursday, May 8, 2008

Scribe Post

Hey everyone, my apologies for the late post (I just got home). But on with the post!

Today was a double class day, and in the morning we went over the spreadsheet on Jess' truck problem., and how to calculate the Present Value of a lease loan.

After that we went over last night's homework and used the spreadsheet as well to solve that problem. If you haven't noticed, there is a link underneath May 7's slides for you to use the spreadsheet at home.

At the beginning of the afternoon class we continued by comparing what happens to the monthly payments and total interest when you change the percentages, and when you change the amount of payments (length of loan). We found out that changing the percentages for the same loan does not significantly affect the monthly payments, or the total interest paid. However, if you change the length of the loan, you will get much bigger changes:

- On a shorter loan, i.e. 3 years, your monthly payments will be higher, but the total interest paid will be smaller.

- On a longer loan, i.e. 5 years, your monthly payments will be smaller but you will end up paying a lot more interest in the long run.

We were then left with Ted's truck to work on class, and whatever you did not finish in class is tonight's homework. Good luck to all!

And for tomorrow, Melissa can have the honors of scribing.

Today was a double class day, and in the morning we went over the spreadsheet on Jess' truck problem., and how to calculate the Present Value of a lease loan.

After that we went over last night's homework and used the spreadsheet as well to solve that problem. If you haven't noticed, there is a link underneath May 7's slides for you to use the spreadsheet at home.

At the beginning of the afternoon class we continued by comparing what happens to the monthly payments and total interest when you change the percentages, and when you change the amount of payments (length of loan). We found out that changing the percentages for the same loan does not significantly affect the monthly payments, or the total interest paid. However, if you change the length of the loan, you will get much bigger changes:

- On a shorter loan, i.e. 3 years, your monthly payments will be higher, but the total interest paid will be smaller.

- On a longer loan, i.e. 5 years, your monthly payments will be smaller but you will end up paying a lot more interest in the long run.

We were then left with Ted's truck to work on class, and whatever you did not finish in class is tonight's homework. Good luck to all!

And for tomorrow, Melissa can have the honors of scribing.

Wednesday, May 7, 2008

Scribe Post

Alright, so basically we only had half of the class since we had a Grad assembly. In the last half of the class we looked over the homework we had to do last night:

Last Night's Homework

Jess also looks at the of leasing the vehicle for 3 years. The price is $24 950.00 plus PST (7%) and GST (5%). The residual value (i.e. the "buyout price") is set at 48% of the new price. The down payment is $2 250.00 and the interest rate is 8.75%.

(a) What is Jess' monthly lease payment?

(b) How much does Jess pay for the lease in total.

(c) If Jess decides to buy the truck at the end of the lease and makes a 2 year loan at 8% to pay the buy-out price, what is the total cost of the truck for her?

Last Night's Homework

Jess also looks at the of leasing the vehicle for 3 years. The price is $24 950.00 plus PST (7%) and GST (5%). The residual value (i.e. the "buyout price") is set at 48% of the new price. The down payment is $2 250.00 and the interest rate is 8.75%.

(a) What is Jess' monthly lease payment?

(b) How much does Jess pay for the lease in total.

(c) If Jess decides to buy the truck at the end of the lease and makes a 2 year loan at 8% to pay the buy-out price, what is the total cost of the truck for her?

We also talked about the positives and negatives (Pros/Cons) of buying and leasing a car. The following image is a table of some pros/cons of buying or leasing of a car. These could also be used to help give a reasoning in questions that are given to you, (i.e. "Would it be better to buy the car or lease it." It all depends on personal preference.)

I hope this will help you understand more about personal finance. Comments are appreciated.

The next scribe will be..... . : : Яέήάή : : . .

The next scribe will be..... . : : Яέήάή : : . .

Tuesday, May 6, 2008

Buying Vs. Leasing, Scribe Post, May 6th

Hey Guys! So I'm the sexy(ehem) scribe today. Good thing we only had the morning class or else my scribe would have been longer than it should be. So, in class we talked about BUYING or LEASING a car. Mr. "K" told us that when LEASING a car or computer, that means we are renting an item owned by the lessor. We, the lessee, we must make bi-weekly or monthly payments to pay for the following:

THE 3 THE's

Also, when we lease a (for example a car), we need to sign a lease agreement.

This agreement specifies 6 things:

Whether it'd be BUYING or LEASING a car, it all depends on the price of the car and how it cost and how it should be paid.

We did one example in class where we were asked to find Jesse's monthly payments and the total cost of the truck.

I'll show you step by step how we get the answer in an organized way(ehem ehem).

Alright, that's all I could do to help you guys. I hope you learned something. Comments are welcome(maybe).

Next scribe is, ADAMSON(Chunkynator)

THE 3 THE's

- The depreciation of the item

- The sales taxes on the amount of depreciation

- The interest on the unpaid value of the item

Also, when we lease a (for example a car), we need to sign a lease agreement.

This agreement specifies 6 things:

- The initial value of the item

- The buy out price at the end of the lease

- The down payment (if there is one)

- The interest rate

- The monthly payment

- Any additional fees

- A car lease will specify how many kms. you can drive

- The fee per km. if you exceed this limit.

Whether it'd be BUYING or LEASING a car, it all depends on the price of the car and how it cost and how it should be paid.

We did one example in class where we were asked to find Jesse's monthly payments and the total cost of the truck.

I'll show you step by step how we get the answer in an organized way(ehem ehem).

Alright, that's all I could do to help you guys. I hope you learned something. Comments are welcome(maybe).

Next scribe is, ADAMSON(Chunkynator)

May 5th Scribe Post

Hey guys, this is my 3rd scribe post..

Today we mostly got caught up in conversations about different things and with the firedrill..

Other than that we went through a couple of warmups and onto a new aspect on our current unit of personal finance.

The lesson we started to learn today was about owning or leasing cars - which one would be better to do?

One of the warmups we started off with was this one on loans:

You start off by inputting the data that you know into the correct places in application TVM Solver.

In this problem, we are given the:

PV ($8250 loan);

I% (8.9%)

P/Y C/Y (compounded monthly)

N (loan repaid in two years [ 24 monthly payments ])

Remember that PV is kept as a positive number this time because since you are loaning money, you are GAINING money that's practically in your pocket rather than investing money that won't be in your pocket.

Use the solve function to find the monthly payment for the loan (PMT).

To find the COST OF THE LOAN multiply the PMT (that you just found) by the # of payments.

To find the INTEREST PAID take the cost of the loan (that you also just found) and subtract it by the previous value (PV).

On these car problems~~ You have to keep in mind that:

When buying a car... You MUST pay;

PST (7%) + GST (5%) when purchasing a NEW car [ 12% tax total ] &

PST (7%) ONLY when purchasing a USED car.

Let's look at the first problem that was given to us on this lesson..

(#1)

Jeff had to pay $21616

-Simply, Jeff is buying a NEW car (12% tax) and selling off his older car to a dealership or somewhere.

-Remember to calculate taxes he must pay AFTER subtracting the cost of the Dodge first because he only has to pay tax on the new Chevy truck that he is buying, not something he is trading in.

***$19300 is being multiplied by 1.12 because that is 12% OF the value + the current value so you won't have to do extra steps on your calculator.***

(#2)

The car is worth 32.77% of it's original value in 5 years.

(since the value of the car was not given we found the % of what the car would be worth instead)

-Because the car constantly decreases in value by 20% every year (due to the way things are in this world) , what's left of the car's value each year is 80% of it...

-So you take 100, multiply it by 0.80 (80%) five times to get the answer for 5 years.

And think about it, if it decreases in value 20% every year, it WON'T be worth nothing in 5 years because its always dealing with a different number. Not stacking up the 20%'s up to 100% of the value.

That's it, that's all.

Thanks for volunteering as the next scribe . . . .

iam.wil

Monday, May 5, 2008

Friday, May 2, 2008

Scribe Post May 02

Today we go over the quiz that we did yesterday. Here are the answer for the quiz:

a)N=120 b)N=60

I%=4 I%=5

PV= -370000 PV=20000

PMT=0 PMT= -377.42

FV=551608.09 FV=0

P/Y=12 P/Y=12

C/Y=12 C/Y=12

c) N=60 d)N=60

I=3.8% I%=3.8

PV=0 PV= -238960.6

PMT= -(4000-377.42)= -3622.58 PMT= -4000

FV=244457.4 FV=559378.08

P/Y=12 P/Y=12

C/Y=12 C/Y=12

Next scribe is CJ...

a)N=120 b)N=60

I%=4 I%=5

PV= -370000 PV=20000

PMT=0 PMT= -377.42

FV=551608.09 FV=0

P/Y=12 P/Y=12

C/Y=12 C/Y=12

c) N=60 d)N=60

I=3.8% I%=3.8

PV=0 PV= -238960.6

PMT= -(4000-377.42)= -3622.58 PMT= -4000

FV=244457.4 FV=559378.08

P/Y=12 P/Y=12

C/Y=12 C/Y=12

Next scribe is CJ...

Personal Finance Blog Assignment 1b

Reply to the question below in the comments to this post. You must include your first name when you publish your reply. If you wish, you may instead choose to answer the problem published as Personal Finance Blog Assignment 1a

You MAY NOT COPY a response published by a student before you. Be creative and create a new or different scenario of your own.

If necessary, click on the image to enlarge it.

You MAY NOT COPY a response published by a student before you. Be creative and create a new or different scenario of your own.

If necessary, click on the image to enlarge it.

Personal Finance Blog Assignment 1a

Reply to the question below in the comments to this post. You must include your first name when you publish your reply. If you wish, you may instead choose to answer the problem published as Personal Finance Blog Assignment 1b

You MAY NOT COPY a response published by a student before you. Be creative and create a new or different scenario of your own.

If necessary, click on the image to enlarge it.

You MAY NOT COPY a response published by a student before you. Be creative and create a new or different scenario of your own.

If necessary, click on the image to enlarge it.

Thursday, May 1, 2008

Alright so i'm the scribe for some reason, but luckily all we did in class is some quiz and for some mythical reason i seem to remember some of the question, I forgot one of the question which is important, I guess the other questions can't be solved.

-So some person is gonna get a sum of cash, but he wants to buy a $20,000 car. His lawyer offers him two options.

Option 1.

pay cash for the car

the rest of $370,000 is invested at a rate of 4% per year, compounded monthly.

Option 2.

Receive $4000 a monthly for the next 10 years

- Finance your car for 5 years with a interest rate of %5 compounded monthly

- Invest the remaining monthly allowance at a rate of 3.8% per year compounded monthly

Basically try to find which is better.

I shouldn't be the scribe but I guess i'll do today because its easy. So the next scribe is Sezy

-So some person is gonna get a sum of cash, but he wants to buy a $20,000 car. His lawyer offers him two options.

Option 1.

pay cash for the car

the rest of $370,000 is invested at a rate of 4% per year, compounded monthly.

Option 2.

Receive $4000 a monthly for the next 10 years

- Finance your car for 5 years with a interest rate of %5 compounded monthly

- Invest the remaining monthly allowance at a rate of 3.8% per year compounded monthly

Basically try to find which is better.

I shouldn't be the scribe but I guess i'll do today because its easy. So the next scribe is Sezy

Subscribe to:

Comments (Atom)

{kind=link}

{kind=link}

{kind=link}

{kind=link}